Deloitte CFO Signals Survey : Key takeaways:

- CFOs’ views on the trajectory of the North American economy improved somewhat; views on Europe and China remain poor.

- Contrary to a year ago, CFOs expect very low interest rates and 10-year bond yields; they again expect a strong U.S. dollar.

- Revenue and capex expectations sit at or near three-year lows; hiring and earnings are among their lowest levels in the last nine years.

- CFOs cite substantial pressure to act on climate change; mostly from their employees, customers, and boards. More than 90% of CFOs say their company has taken at least one action in response to climate change, with the average CFO reporting nearly four.

- Consumer and business spending expectations have fallen; CFOs are less likely to expect higher industry revenue and prices.

Why it matters to CFOs?

Each quarter, CFO Signals provides a unique barometer for how CFOs from North America’s largest and most influential companies view and interpret developments in the global economy. Since 2010, the report has provided key insights on the business environment, company challenges, finance function practices, and CFO career priorities. All participants are CFOs; almost 75% of their companies are publicly traded; and more than 80% have over $1B in annual revenue.

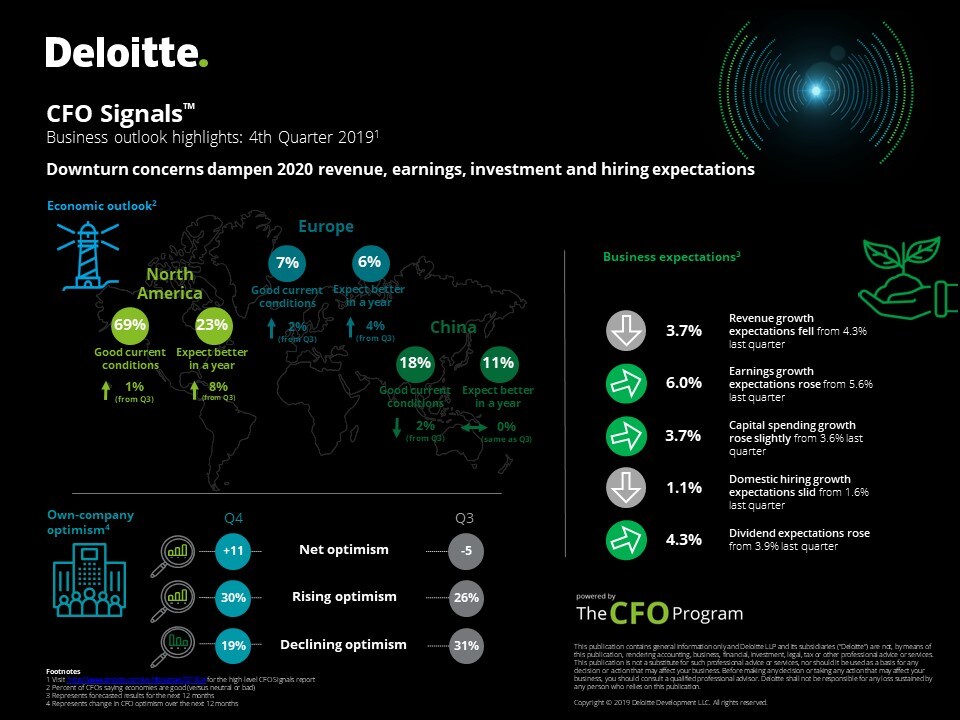

Economic perceptions level off for North America, rise for Europe, but decline for China

Perceptions of North America leveled off, with 69% of CFOs rating current conditions as good (68% last quarter). Assessments of the North American economy rebounded slightly this quarter with 23% of CFOs now expecting better conditions in a year — better, but still the second-lowest reading in more than six years. In terms of perceptions of Europe’s economy, only 7% of CFOs say current conditions are good (up from 5% last quarter), and only 6% expect better conditions in a year (up from last quarter’s survey-low 2%). Perceptions of China’s economy have been mostly declining since early 2019. The proportion of CFOs who say current conditions are good fell from 20% to 18% (a three-year low), and just 11% expect better conditions in a year.

Anticipating a downturn

Expectations for a U.S. downturn have risen since earlier this year, with 97% of CFOs saying that a downturn (a slowdown or a recession) has already begun or will occur by the end of 2020 — well up from 88% in 1Q19. Overall, 12% of CFOs say they believe a downturn has already commenced, and 14% say they already see signs of a downturn in their company’s operations.

In terms of macroeconomic expectations for 2020, CFOs cite falling expectations for consumer and business spending, and two-thirds say performance beyond 2020 will depend substantially on upcoming U.S. elections.

Stakeholder pressure to act on climate change

In terms of addressing climate change, 71% of CFOs say they face moderate or higher pressure from at least one stakeholder group. Overall, the most common sources of higher pressure are employees, customers, boards, and investors (in that order). Furthermore, more than 90% of CFOs say their company has taken at least one action in response to climate change. The most frequently reported: increased efficiency of energy use; including climate risk management in governance processes; and use of energy-efficient or climate-friendly equipment.

Sanford Cockrell III, national managing partner of the U.S. Chief Financial Officer Program, Deloitte LLP said, Compared to early 2019, companies appear to be taking more defensive actions related to downturn expectations—particularly around reducing spending and limiting or reducing headcount. While CFOs expect some form of US downturn by the end of 2020, the good news is that expectations of a full-blown recession have fallen sharply since 1Q19.

Greg Dickinson, managing director, North American CFO Survey, Deloitte LLP said, In coordination with our European colleagues, we examined the pressure companies are under to address climate change. More than 70% of North American CFOs say their company is under substantial stakeholder pressure to act, and more than 90% say they have taken action. Perhaps most importantly, the majority say they are building management of climate risks into their governance processes.

Concerns over political turmoil and talent continue to escalate

This quarter saw even higher concerns about political turmoil, with growing use of the term “instability” and increased mentions of the potential impacts of the 2020 U.S. elections. When it comes to internal risks, CFOs again expressed very strong talent concerns, as well as worries about strategy execution and managing change.

Companies continue to focus on growth and investment

Companies remain more focused on revenue growth than cost reduction (46% versus 33%), but their cost reduction focus hit its highest level in about six years. Their bias toward investing cash over returning it to shareholders continued (47% versus 23%), however their focus on returning cash hit its highest level in about four years.

Capital markets assessments and expectations

With interest rates declining for the past two quarters, debt attractiveness rose to 87% last quarter and held at 86% this quarter — the second-highest level since 3Q16. Seventy-seven percent of CFOs now say U.S. equity markets are overvalued, well up from 63% last quarter and the highest level in nearly two years. Going forward, only 17% of CFOs expect the U.S. federal funds rate to be higher than the current rate (1.5%) at the end of 2020, and just 5% expect to see negative rates by end of the year. Two-thirds (67%) expect the 10-year bond yield to remain below 2%. Similar to a year ago, CFOs are very unlikely to say they expect major global currencies to strengthen against the U.S. dollar. Only about one-quarter believe either the euro or the British pound will be stronger versus the U.S. dollar, and only 21% say the same for the Chinese renminbi.

Growth metrics

Year over year expectations for revenue growth fell from 4.3% to 3.7%, a three-year low; earnings growth rose from 5.6% to 6%, but sits at its second-lowest level in survey history; capital spending growth rose slightly from 3.6% to 3.7%, remaining near its three-year low; and hiring growth slid sharply from 1.6% to 1.1%, the second-lowest level in nearly six years.

To see additional results from Deloitte’s fourth-quarter 2019 CFO Signals survey, download a copy at: deloitte.com/us/cfosignals2019Q4.

{kind=link}