Businesses Bracing for Major Disruptions from COVID-19 according to S&P Global Market Intelligence Survey

Survey Results Found Approximately 79% of Organizations Reported Already Experiencing Negative Impact of COVID-19

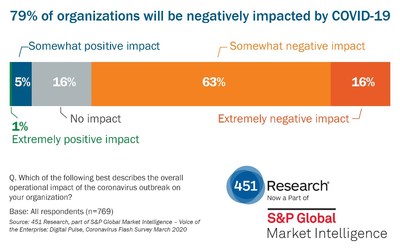

Enterprises around the globe are bracing themselves for major disruptions expected from the impact brought about by the ongoing COVID-19 outbreak, according to a recent survey conducted by 451 Research, the emerging technology research unit of S&P Global Market Intelligence. 63% of respondents say that the COVID-19 outbreak is having somewhat of a negative impact on overall business operations, while nearly 16% report an extremely negative impact. Major business disruptions in organizational supply chains, IT resources, human capital, and strategic planning are contributing causes of the reported negative impact.

451 Research’s Digital Pulse COVID-19 Flash Survey features responses from approximately 820 IT decision-makers across a range of industries. The survey was conducted between March 10 through March 19, 2020 and the results shed light on the difficulties enterprises are currently encountering or expecting to face due to the COVID-19 outbreak sweeping the globe.

Liam Eagle, Research Vice President and General Manager of Voice of the Enterprise, at 451 Research, part of S&P Global Market Intelligence said, “Global enterprises are now dealing with the unknown, navigating a very unique and difficult situation on a daily basis. Our survey results helps delineate the challenges facing these organizations and shares insights on which area of operations will be most impacted in the long-term within their respective industries.”

Highlights from the survey include:

- Many enterprises expect major disruptions to their businesses within six months. 15% of respondents are already experiencing major disruptions or expect one within the month, and that increases to 26% within two months and 51% within six months.

- Companies are expecting to spend more on several key areas of technology. 43% of respondents are expecting to invest more in employee communication and collaboration technology, 37% on mobile devices and services, 32% on bandwidth and network capacity and 28% on information security, among others.

- Impact extends to strategic plans including recruitment and product launches. Enterprises say they have already halted or delayed strategic plans as a result of COVID-19, including hiring staff (34%), new product or services rollout (22%), IT hardware or software refresh (15%) and IT infrastructure buildout (12%), among others.

- Demand on IT resources is increasing but not insurmountable. Among enterprises surveyed, 41% are already experiencing increased strain on internal IT resources, and another 14% expect to begin experiencing it within the next three months. Additionally, 34% of enterprises plan to spend more on IT resources and assets (51% for companies with more than $1bn in revenue).

- COVID-19 will likely have a permanent impact on modes of working. Enterprises surveyed are broadly implementing travel bans, work-from-home policies and limits on internal and external meetings. Many expect these policies to remain in place long term or permanently, including 38% for expanded/universal work from home policies, 23% for travel limitations or bans, and 16% for not attending events they have previously attended.

- Respondents were reacting to rapidly changing circumstances. The situation around the outbreak evolved rapidly while the survey was in field, and we saw responses shift significantly between the earliest group to complete the survey (March 10-11) and the latest (March 18-19). The portion experiencing increased IT strain roughly doubled (24% to 43%), as did the groups seeing loss of customer demand (22% to 40%), reduction in employee productivity (17% to 44%) and reduced materials supply (26% to 32%). Time also had an impact on those expecting to spend more on IT resources (20% to 40%), those spending less on labor (6% to 30%), those that had enacted office closures (15% to 38%) and those claiming they hadn’t delayed or halted any strategic plans (65% to 47%). We expect that these trends continued beyond the conclusion of the fielding.

{kind=link}