Marko Geber

Company Overview

Toast (NYSE:TOST) offers a cloud-based end-to-end POS tech platform primarily focused on restaurant and food services. They offer a broad portfolio of software and payment solutions that help to solve the needs of restaurants. The company’s payment processing offerings are built on charging transaction fees for its restaurant clients for debit and credit card payments on restaurant sales.

Product Overview

Toast offers three broad categories of products for its restaurants:

- Toast Hardware services: A major aspect of Toast services include its Point of Sales (POS) systems, ‘Toast Order & Pay,’ ‘Toast Go,’ and Guest kiosk devices. The Toast Flex system is an integrated solution that can also be purchased with a detachable screen that can face guests to be able to verify order accuracy and improve the customer ordering and payment experience.

- Subscription services: They include Point of Sale subscriptions, Restaurant Operations, Digital ordering/delivery, email marketing & loyalty, and a team management module. Additionally, within this module, they have Platform services that provide customers with Reporting & Analytics, eCommerce, and API Partner Ecosystem.

- Financial Technology Solutions: They include Integrated payment processing, financial technology products

Industry – Verticalized Software

The last decade of software was about the move to the cloud from on-prem. This trend gave rise to software as a service (SAAS) and, therefore, more businesses offering horizontal software services. This success led to the creation and flourishing of giants like Salesforce (CRM) and Oracle (ORCL). Platforms that served multiple verticals and industries with a generalized software solution that met customers’ needs.

After the success of horizontal software over the past decade, we are now experiencing a shift towards more vertical software. Customers within niche industries are beginning to feel that the software solution available within their sector is not personalized and doesn’t cater to their problems. Vertical SaaS is an industry categorized by software companies that provide a custom solution for a specific industry or category. There is a big opportunity for software to penetrate many industries that haven’t traditionally had software purposely built for their vertical.

In many cases, the total addressable market opportunity for these industries might appear tiny at the onset but, over time, they expand as more of the sector sees the productivity or cost savings that can be enhanced by incorporating software into their internal process. Beyond Toast which we will discuss, many other industries such as construction have seen this success with companies like procure (PROR). On average, companies spend 5% of their sales on technologies. It means that a vertical SaaS with the all-in-one platform can likely charge up to 5% of the revenues generated by its customers.

Before 2011/2012, when platforms like Toast, Square (SQ), and Lightspeed were successful. Many restaurants lagged in technology adoption, with many continuing to rely on manual processes for taking orders, managing operations, and coordinating with staff. Many restaurants would take orders through the phone or with pens and paper. The few that utilized any technology used legacy systems that did not successfully scale at large.

As of today, Toast’s comprehensive hardware and software assist restaurants in running almost all the operations for their restaurant, from streamlining operations to improving the customer experience. Businesses have been able to modernize invoice processing by eliminating manual data entry and invoice scanning by implementing Toast’s xtraCHEF. Additionally, businesses adopting Toast Order & Pay have been able to streamline the ordering and payment process by doing everything from their mobile phones. Overall, restaurants have been able to automate more of their operations and save time and effort by improving efficiency. Restaurants are able to focus on managing operations and enhancing the customer experience and employee productivity.

Investment Thesis

- Large Total Market Opportunity (‘TAM’): Toast is one of the key leaders within a large market. The total restaurant for the US is around $55B with a sector addressable market of over $15B. Toast says there are over 860,000 restaurants in the United States. Toast averages about 1.7-2.0 locations per restaurant. The company has a big opportunity ahead of them to expand this TAM by 1) Penetrating other verticals such as other retail, delivery services, or sectors that are adjacent to restaurants. (2) expanding internationally to new geographies around south and central America. and lastly, (3) continue to capture market share gains from legacy competitors.

- Unique Go-To-Market Strategy: The company’s Go-To-Market strategy is focused on a hyper-localized strategy, i.e., Toast is usually focused and tailored on local and suburban regions based on the unique characteristics of that location. It usually aims to grow its location base and cross-sell more software modules through a “land and expand” strategy. Toast also relies heavily on word of mouth and referrals in its strategy.

- Toast Capital and Credit Opportunity: Toast Capital, which is a merchant cash advance, a similar product to that provided by SQ Capital. Since Toast sees everything about the customers, they have the ability to underwrite loans at much more efficient pricing for their customers. SMB loan is an opportunity for the company.

- Competitive moats and earnings catalyst: The company has a variety of competitive strengths and earnings catalyst that positions the company to outperform over the next 12-18 months.

Competitive Moats

Most comprehensive software suite: Toast provides the most comprehensive end-to-end solution for restaurants compared to its competitors. Toast’s fully bundled suite encompasses everything from hardware to software that a restaurant would need to operate their entire operations on the platform.

Brand Recognition: Across major US restaurants, Toast is one of the most recognized software payment providers. Although it is difficult to estimate the exact numbers, Toast, Olo (OLO), and Square have the largest land grab.

Switching Cost and Mission Critical: Once a restaurant installs Toast’s software across their operations, i.e. from POS systems to payroll, team management, and more, it is difficult for a restaurant to unbundle it right away. If Toast’s systems were to break down completely, it could cost a restaurant loss in revenue since that business could suffer from lost processing card payments and managing online orders. The net dollar retention has been over 110% in the last 5-years which provides proof of its stickiness to merchants.

Strong Partner Network: Toast has a large ecosystem network of over 150 third-party partners that integrate and help simplify the implementation of the Toast platform. The partner ecosystem consists of large players like Doordash (DASH), accounting to payroll solutions. One of the core principles of the founders was to ensure that the platform could integrate with multiple technology systems since every restaurant has different needs. This broad array of ecosystem networks, specifically within the restaurant industry, is a core competitive advantage for Toast that makes it hard for competitors to easily replicate overnight. Additionally, customers will always go with the software provider that integrates with a wide variety of partners.

Favorable Competitive Position: Toast’s key competitors include National Cash Register (NCR), Oracle’s Micros restaurant software, Square, Olo, and Lightspeed. NCR and Oracle have a decent market share in the existing industry, but those platforms are primarily legacy platforms that are not cloud-native platforms. Toast’s platform is cloud-native and therefore allows for quick system updates, and it can be easily configurable for each restaurant’s needs.

Olo is more about providing food ordering and delivery services through an integrated software system. Square and Lightspeed are the closest competitors to Toast’s platform. The key differentiators for Toast are that they have a platform that they have a unique 24/7 hour service customer support for all their businesses, and they place it as a priority that when restaurants struggle, Toast will provide the answers to your questions.

Financial Model

Below are the key financial metrics to track and measure the investment thesis:

Recurring Revenues: TOST generates most of its revenue from software subscriptions, payment processing – financial technology solutions, and Toast hardware sales. The software subscription, including the payments revenue, is the relevant metric when evaluating the growth and margin profile of the business. TOST intentionally sells its hardware and professional services at a negative gross margin since management believes the hardware and services as customer acquisition costs for long-term lifetime value.

Toast outperformed many of its peers during the depth of the 2020 pandemic, and in its most recent quarter, the growth outperformance provides the company’s resilience and differentiating factors. In 2020 and 2021, the business saw a higher shift towards higher margin card-not-present and debit card transactions during the peak of the pandemic.

Toast generates ~60% of its recurring revenue from payment processing, with the rest coming from software priced on a subscription basis and over 40% coming from software subscriptions. The software component creates a consistent revenue stream that is balanced with the volatile payments revenue.

Gross Profit: This is the key metric to value the business. Toast’s hardware and professional services are intentionally priced at negative gross margins to ease the implementation and onboarding process for new customers. This makes the gross margins look very low, mid 30’s that are reported under GAAP.

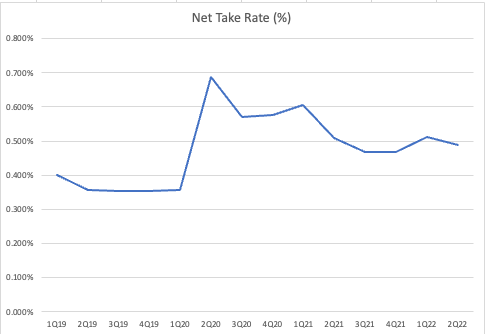

Net Take rate: The net take rate takes into consideration the payments revenue derived from the GPV. As an observation, the metric was high during the pandemic because during the height of the pandemic online food ordering spiked, and consequently, Toast’s take rate improved, as take rates are generally higher for online orders. Also, with a large increase in the use of debit cards during that period, Toast earned higher spreads per transaction.

Toast Investor Relations/Authors Calculations

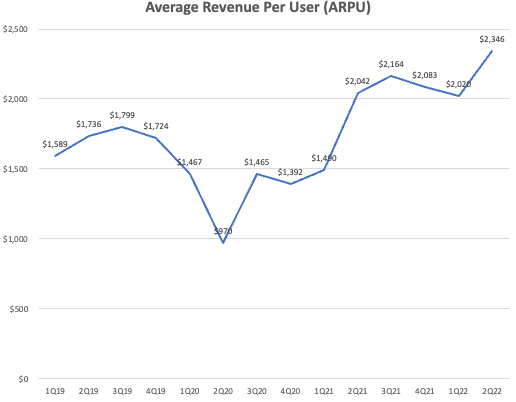

The average revenue per user: This measure calculates the ARR (Annual Recurring Revenue) divided by the number of locations within Toast’s ecosystem. The average revenue per location has increased over the past couple of quarters as Toast is able to derive more revenue from its average store.

Toast Q2 Earnings/ Authors Calculation

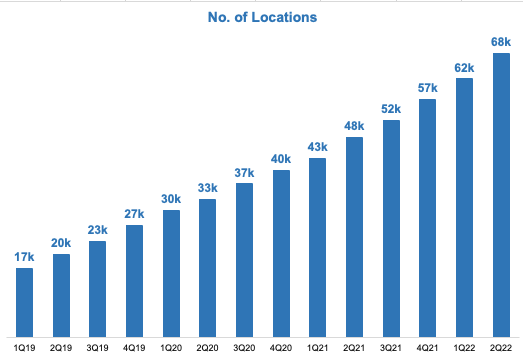

The number of locations adopting Toast: The growth in the number of locations is another key measure to watch. As observed, the number of restaurants has continued to grow, 42% year-over-year, and showing a 10% quarter-over-quarter growth.

Toast Q2 Investor Presentation / Authors Calculations

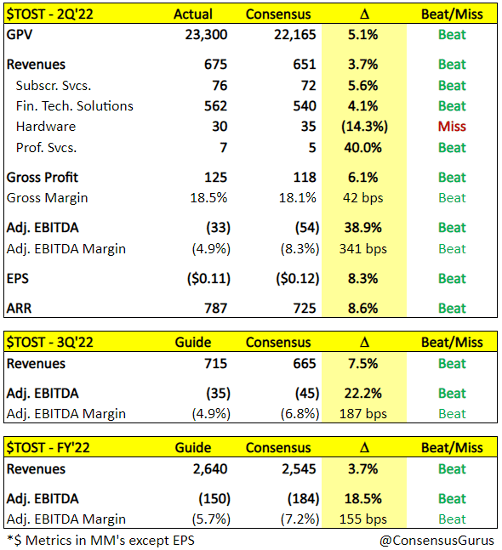

Q2 Earnings Highlights

Toast recently had a great earnings quarter. They beat all their metrics across the board. Most surprising to the street was the 7.5% increase in guidance to third quarter revenues, 22% EBITDA beat, and the raising of the full-year guidance by 4%.

This is in full contrast to Olo, which guided to a -0.4% for Q3 2022 and -8.1% for the FY 2022.

ConsensusGuru Twitter Account/Factset Estimates

Management Team

Toast is led by Chris Comparato as its CEO. He has a wealth of experience spearheading successful SaaS companies. The company was founded by Jonathan Grimm, Aman Narang, and Stephen J. Fredette in 2011 and is headquartered in Boston, MA. Additionally, they are currently still founder-led, with all three co-founders (MIT graduates) in top executive roles at the company. Management still has over 11% ownership which is a strong amount of ‘skin in the game’.

Risk Factors To The Thesis

- Unprofitable and Free Cash Flow Negative: The business is still not currently profitable due to product development and growth investments. The company is more susceptible to interest rate risk as the market discounts its cost of capital.

- Supply chain risks: The ongoing supply chain/chip shortages could result in hardware bottlenecks for Toast, could extend implementation times, and delay customer onboarding which could affect the company’s growth.

- Competitive Industry: While Toast holds a strong competitive position, there is intense competition from existing players such as Square, NCR and Lightspeed, and Oracle’s Micros which could siphon or slow down growth. Additionally, there is always the opportunity for competitive pressures could affect Toast’s ability to maintain a brand recognition advantage in the restaurant space.

- Consumer spending and recession risks: There is always a potential that a recession combined with low consumer spending could affect net new SMB restaurant openings or present significant churn at the SMB restaurant level. These are factors that affect Toast’s future growth prospects.

Summary

Restaurants have lagged in technology adoption, with many continuing to rely on legacy systems and haven’t realized the full benefits of using a cloud-native platform. Toast’s platform helps restaurants in managing operations, drive down costs, and optimize for growth. Toast is riding the waves of vertical software. Among other achievements, they were most recently named Forbes #1 POS system of 2021 and 2022 for cafes. Finally, in the near term, the company’s optimistic beat and raise, together with analyst estimates revising higher, is a signal that the business should continue to enjoy key tailwinds.