The slowdown in China, floods in Pakistan and the uncertain global economic environment have had severe economic impacts on the APAC region, significantly increasing risk to investors doing business in the area, according to GlobalData. Research by the leading data and analytics company has revealed that the APAC region’s level of investment risk rose by 2.4% in one quarter.

The research was conducted as part of GlobalData’s ‘Global Risk Report Quarterly Update – Q3 2022’ report, which outlines its Country Risk Index (GCRI). This model analyses a number of economic factors and calculates the amount of risk an investor accepts when doing business in each country and region worldwide. This is then represented by an overall ‘score’. The APAC region’s risk score was 41 in Q2 and this rose to 42 in Q3.

Puja Tiwari, Economic Research Analyst at GlobalData, comments: “The APAC region is experiencing a slowdown in 2022 amid an uncertain global environment, high inflation, financial tightening, and supply chain disruption. The relatively sluggish growth in China is also affecting growth prospects in the region more widely. Hong Kong, Singapore, Japan, Vietnam, South Korea, and India accounted for 28.4% of Chinese exports in 2021, and these countries remain vulnerable to China’s supply chain woes.

“Further, the overall APAC region continues to face political and economic risks caused by the worst flood in Pakistan since its independence, alongside a spiralling economic crisis in Sri Lanka.”

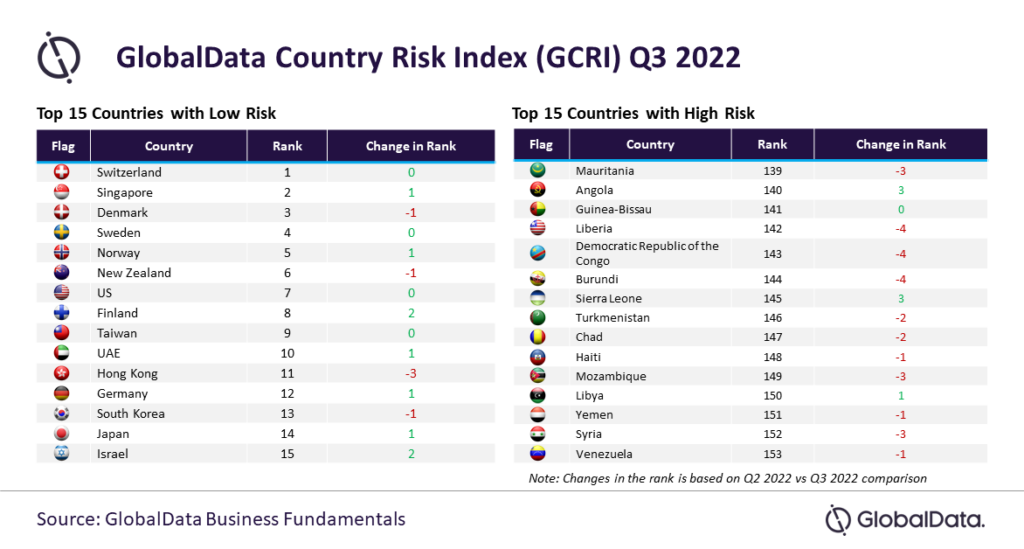

GlobalData’s report reveals that Pakistan, Myanmar and Turkmenistan are on the list of the highest-risk nations worldwide in Q3 2022. However, Singapore, New Zealand, and Hong Kong are on the list of the top 15 lowest-risk countries worldwide for Q3.

Tiwari continues: “The overall APAC region continues to face political and economic risks in the form of geopolitical tensions in the South China Sea, spikes in price levels, and the consequent supply chain disruptions.”

Looking more broadly, GlobalData’s report highlights that global risk increased from 44 out of 100 in Q2 2022 to 44.9 in Q3 2022.

Tiwari adds: “The major causes of risk worldwide include the price rises as a result of the Russia-Ukraine war and sanctions on Russia, the energy crisis in Europe, a slowdown in China’s growth, aggressive interest rate hikes by central banks, depreciating currencies, and a crashing stock market.

“While governments of major economies are undertaking various fiscal measures to deal with the rising prices, this will weigh on already strained government finances. Moreover, with several economies tightening monetary policy, the increasing borrowing costs will remain another challenge moving into Q4 and beyond.”

{kind=link}