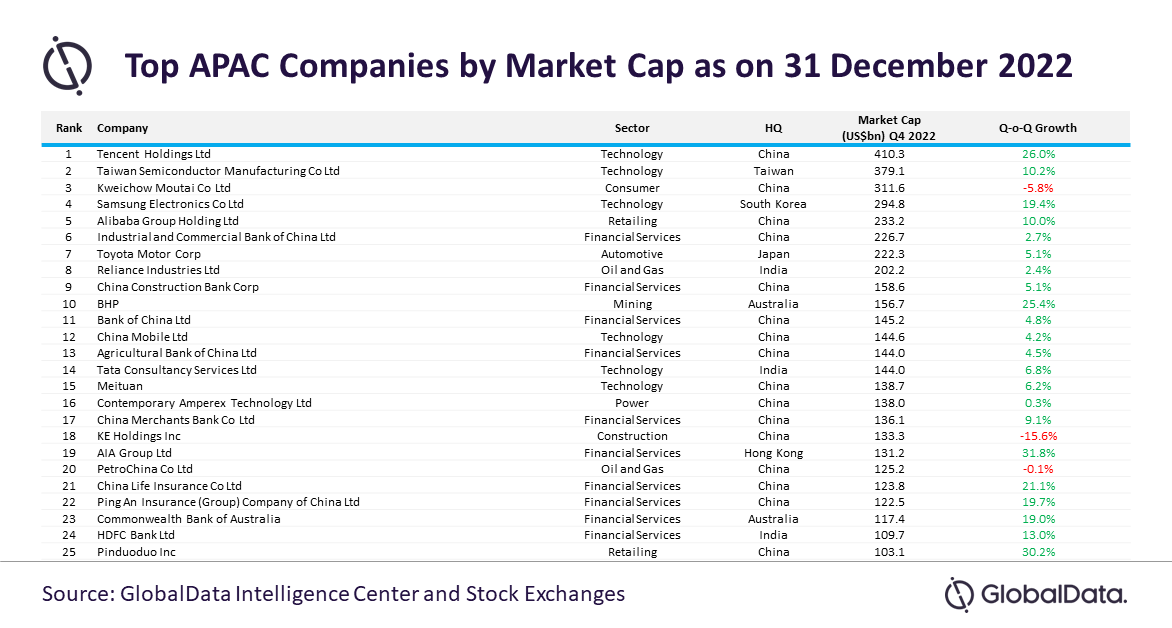

Amidst the high inflation environment, geo-political tensions, and higher interest rates, the aggregate market capitalization (MCap) of the top 50 Asia-Pacific (APAC) companies grew by $519 billion in the fourth quarter (Q4) of 2022 (as of 31 December 2022), reveals GlobalData, a leading data and analytics company.

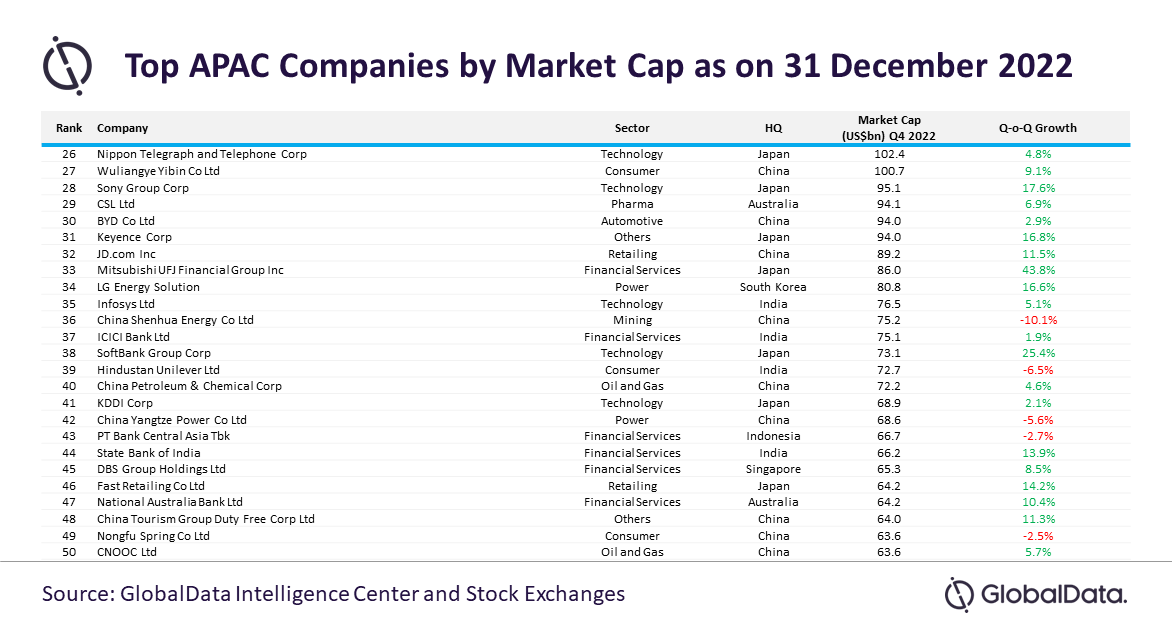

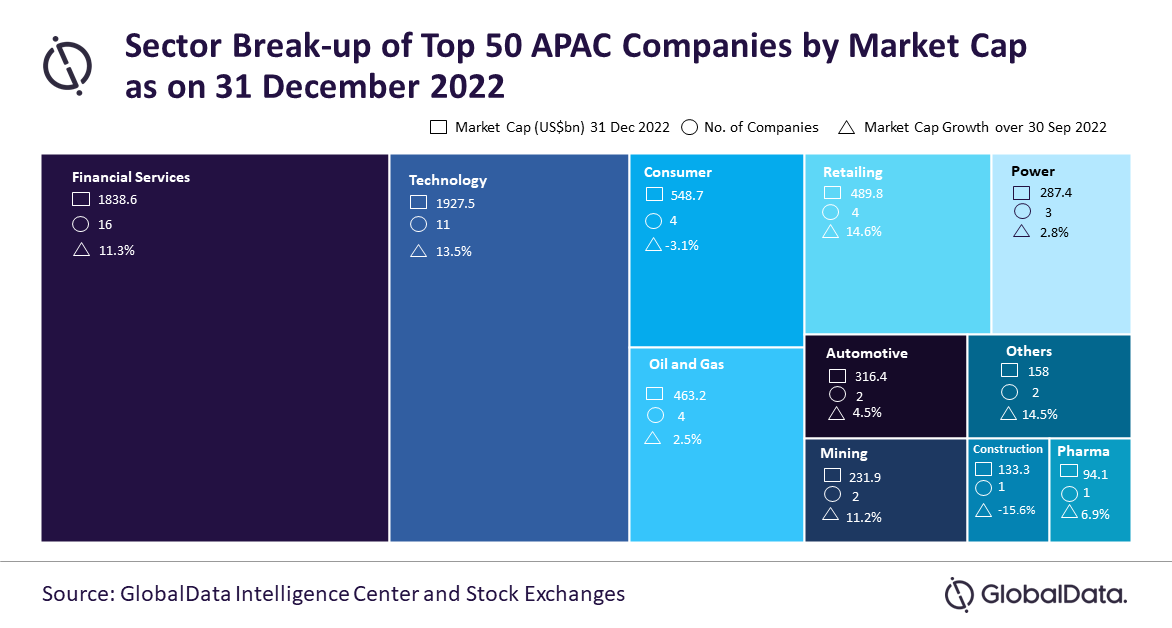

Financial services and technology sectors topped the list with an aggregate market valuation of $1.8 trillion and $1.9 trillion, respectively. The top 50 list includes 16 companies from the financial services sector and 11 from the technology sector. In terms of geographic split, 25 firms are from China, followed by eight from Japan and seven from India.

Mitsubishi UFJ Financial, AIA Group, Pinduoduo, Tencent, BHP, and Softbank witnessed the highest quarter-on-quarter (Q-o-Q) growth of more than 25%, whereas KE Holdings and China Shenhua Energy saw their MCap eroding by more than 10%.

Murthy Grandhi, Business Fundamentals Analyst at GlobalData, comments: “In Q4, 85% of the top 50 companies saw their MCap increasing from the previous quarter. Easing of China’s zero-COVID policy and regulations on internet companies, and Beijing’s government supportive measures on embattled property sector immensely contributed to the recovery of Chinese capital markets.”

Mitsubishi UFJ Financial rallied owing to its positive performance in H1 FY2023 (30 September 2022). In line with its integrated health strategy, AIA Group demonstrated a more than 30% increase in MCap above favourable Q3 2022 results, and as part of its bull run, it implemented inorganic expansion initiatives like the purchase of Blue Cross and MediCard.

China’s e-commerce firm Pinduoduo’s third-quarter performance outpaced the market estimates, which resulted in 30% surge in MCap, while gaming giant Tencent rallied on the back of regulatory easing on internet firms.

Grandhi adds: “Chinese housing company KE Holdings reported a 15% decline in MCap owing to macro headwinds, disruption in the recovery of the housing market caused by the resurgence of COVID-19 in certain regions, and many real estate developers were facing liquidity challenges. Mining giant China Shenhua Energy continued its bearish trend because of 18% decline in coal sales in Q3 2022.”

Among the Indian firms, HDFC Bank and State Bank of India had a positive momentum after recording healthy overall financial performance numbers and lower non-performing assets in Q2FY23 coupled with easing of monetary policy and expectations of revival in economic activity.

Grandhi concludes: “2023 will remain volatile at least during the first half of the year; but the region will remain a bright spot amidst the slowing global economy, forex strain, and weak Chinese recovery. Rise in domestic demands and inbound tourism, easing of supply chain disruptions, regional free-trade agreements, and declining commodity prices could fuel the growth in the region.”