BANGKOK–(BUSINESS WIRE)–FICO (NYSE: FICO), a leading global provider of analytics software, today announced further findings from its consumer fraud survey exploring attitudes and preferences towards fraud checks. The study revealed that almost half of Thais are willing to commit fraud to obtain a loan or file an insurance claim. However, it also highlighted that financial institutions can generate increased revenue and drive sales through a successful fraud protection function.

More information:

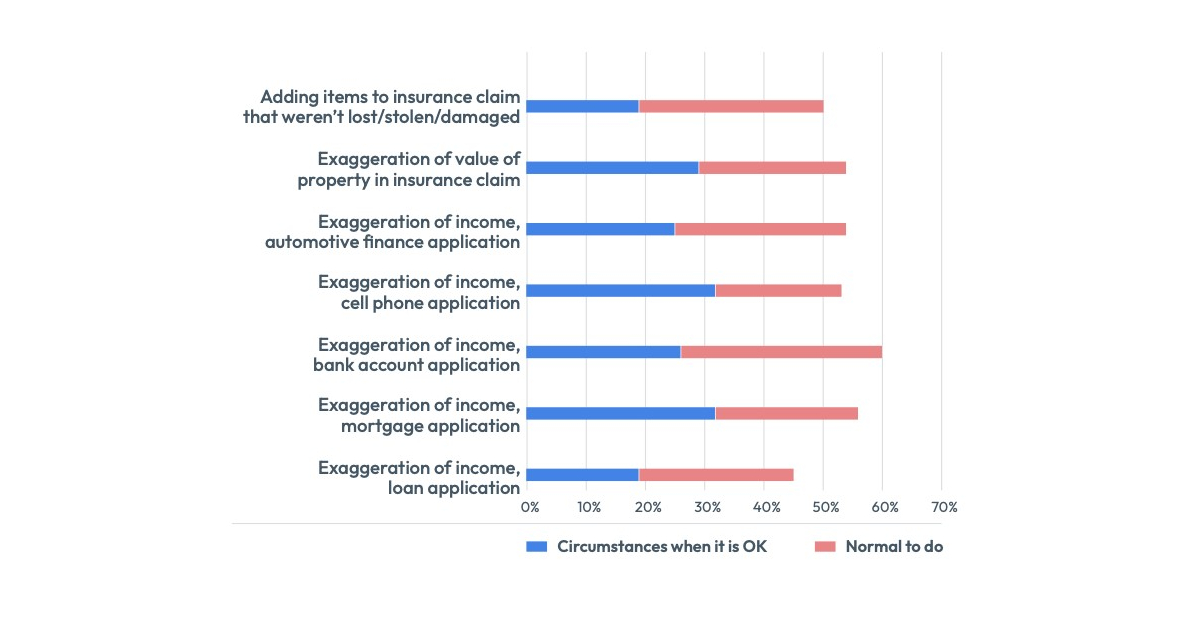

Giving false information is considered acceptable by many

When asked about their attitudes to giving false information for financial or material gain – known in banking as first-party fraud – half of Thais supported these behaviors. Around 25 percent of respondents said there are circumstances when it’s OK to exaggerate income on a loan or mortgage application, while 25 percent thought it was normal to do so. The survey revealed similar proportions of consumers would exaggerate an insurance claim or add items to a claim.

“The willingness to commit fraud for financial gain is concerning, it signals a strong need for Thai banks to bolster their fraud prevention models,” said C.K. Leo, FICO’s lead for fraud, security and financial crime in Asia Pacific. “A robust fraud prevention strategy would not only safeguard customers’ interests but also strengthen the bottom line of businesses.”

This sentiment is consistent with Southeast Asian neighbors Indonesia and The Philippines, and interestingly even more pronounced in Malaysia where over 60 percent of the respondents said such behaviors are normal.

The results indicate that banks in Thailand may be making inaccurate risk assessments as a result of false information on applications, potentially leading to financial losses from inflated insurance claims. Additionally, customers may not be aware that providing incorrect information on applications or claims is illegal.

“The gloomy economic situation, made worse by the rising cost of living, has driven some Thais to desperate measures for credit access. Nevertheless, this cannot justify fraud,” said Leo. “By improving their ability to detect misrepresentation of information, financial institutions can safeguard themselves against losses from bad debt, while steering customers away from regrettable paths.”

Fully leveraging data and analytics to drive fraud protection

Financial institutions frequently possess the evidence required to distinguish between fraudulent and legitimate applications. However, fraud teams are frequently unable to utilize this data because it is siloed. These inefficiencies result in inadequate fraud protection and compromise the customer experience. Banks prompt customers with arduous and time-consuming identity checks, resulting in increased costs and duplications that cause frustration for customers.

“Given the region’s competitive banking landscape, utilizing the wrong fraud strategy can be costly,” said Leo. “To achieve success, fraud teams must strike a balance between strong fraud protection and meeting the legitimate needs of customers. This can be achieved through a holistic approach to applicant data, which enables effective differentiation between fraudulent and legitimate applications. The use of analytics and machine learning models will further bolster a bank’s fraud defenses, leading to better customer satisfaction.”

Conducted in late 2022, the report surveyed 1,000 people each in 14 countries: Thailand, the USA, Canada, Brazil, Mexico, Colombia, Peru, Malaysia, The Philippines, Indonesia, South Africa, Germany, the UK and Sweden.

About FICO

FICO (NYSE: FICO) powers decisions that help people and businesses around the world prosper. Founded in 1956, the company is a pioneer in the use of predictive analytics, AI and data science to improve operational decisions. FICO holds more than 200 US and foreign patents on technologies that increase profitability, customer satisfaction and growth for businesses in financial services, manufacturing, telecommunications, health care, retail and many other industries. Using FICO solutions, businesses in nearly 120 countries do everything from protecting 2.6 billion payment cards from fraud, to improving financial inclusion, to increasing supply chain resiliency. The FICO® Score, used by 90% of top US lenders, is the standard measure of consumer credit risk in the US and other countries, improving risk management, credit access and transparency.

Learn more at http://www.fico.com.

Join the conversation at https://twitter.com/fico & http://www.fico.com/en/blogs/

For FICO news and media resources, visit www.fico.com/news.

FICO is a registered trademark of Fair Isaac Corporation in the US and other countries.