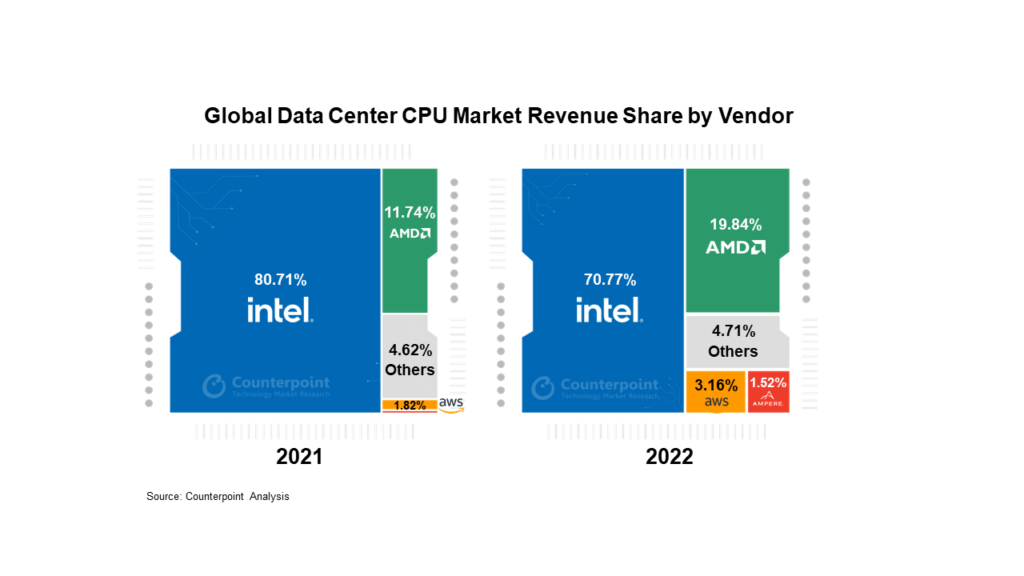

- The global data center CPU market’s revenue declined 4.4% YoY in 2022.

- AMD registered a 62% YoY growth in its data center CPU revenue to hold a 20% market share.

- Intel’s data center CPU revenue dropped by 16% YoY in 2022, while its market share fell to 71%.

- ARM-based CPUs gained traction with Ampere, Graviton (Amazon) and Yitian (Alibaba) to surpass $1 billion in revenues for the first time.

The global data center CPU market’s revenue registered a 4.4% YoY decline in 2022, according to the latest research from Counterpoint’s Semiconductor Service. Macroeconomic headwinds and increased energy costs impacted the sales of data center CPUs during the year. Besides, from the architecture perspective, the addition of accelerators in the servers for workloads restricted the demand for additional CPUs for servers.

Commenting on the companies’ 2022 performance, Senior Research Analyst Akshara Bassi said, “Even though Intel is still the market leader, its market share loss points to AMD’s rising product portfolio and better performance over Intel. AMD surpassed Intel in market share growth in 2022. Intel suffered due to continued delays in the release of its next-generation product Sapphire Rapids, generationally comparable to AMD’s Milan launched in 2021.

As demonstrated by hyperscalars AWS and Alibaba, ARM-based architecture chips continue to gain steam due to the ROI offered on varied workload deployments and off-the-shelf solutions from Ampere Computing, and shipping of data center CPUs from NVIDIA in H1 2023.”

Talking from the foundry perspective, Associate Director Dale Gai said, “As evidenced by wafer demand and foundry capacity of advanced nodes from TSMC, the total wafer sales at 5/4nm rose by 85% YoY in 2022. One of the demand drivers for the increased demand of advanced nodes is data center CPUs”

Market summary for 2022

Intel remained the market leader with a 71% share, although far from the share that it commanded till 2018. Its revenue from the segment dropped 16% YoY in 2022. The market share declined primarily due to delays in next-generation products and weakness in enterprise spending due to macroeconomic conditions.

AMD came second with a 20% market share primarily driven by increased adoption of its EPYC processor Milan. AMD is becoming a dominant force in the x86-based CPU for data centers, being increasingly adopted by cloud providers and SKUs of server companies. AMD registered a 62% YoY growth in its data center portfolio in 2022.

AWS’ in-house ARM-based chip Graviton, now in its third generation, has been among the early adopters of ARM architecture in a data center. AWS has increased Graviton’s penetration in its offerings and also expanded it to support ML-based instances with in-house accelerators, representing a shift from general-purpose compute to specific workloads.

Ampere Computing started to gain more traction in 2022 with its expansion from traditional cloud providers to enterprises by having its CPU in off-the-shelf servers from OEMs.