Amidst the recession fears, geo-political tensions, higher interest rates, prolonged lockdowns and a slump in technology stocks, the aggregate market capitalization (MCap) of the top 50 Asia-Pacific (APAC) companies declined by $900 billion in the third quarter (Q3) of 2022 (as of 30 September 2022), reveals GlobalData, a leading data and analytics company.

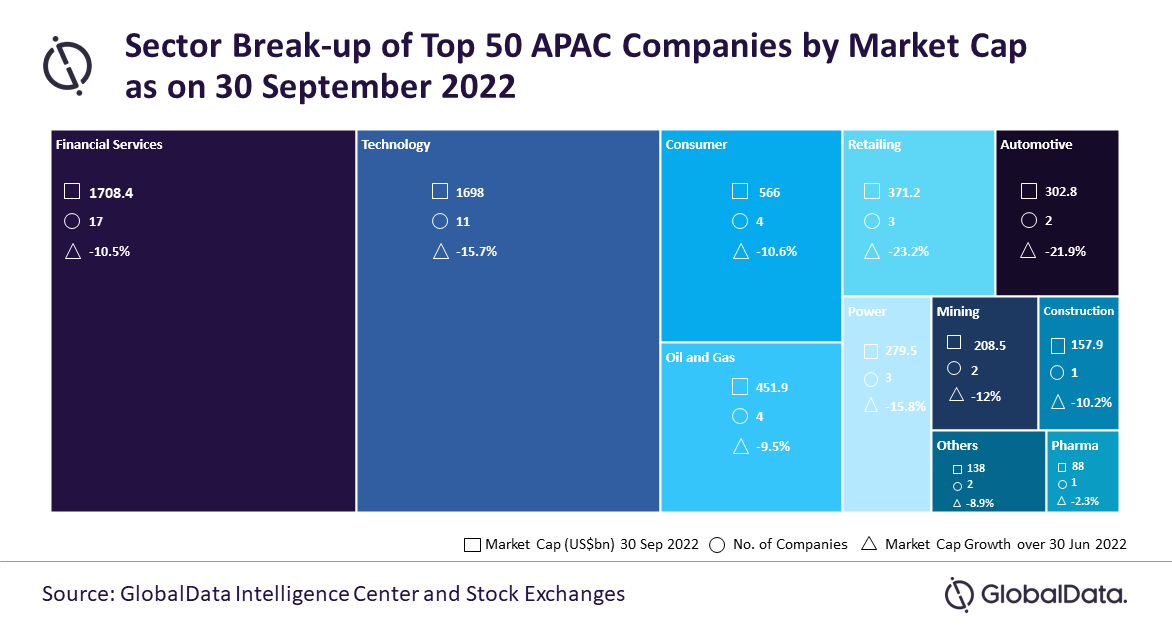

Financial services and technology sectors top the table with an aggregate market valuation of $1.7 trillion each. The top 50 list includes 17 companies from the financial services sector and 11 from the technology sector. In terms of geographic split, 26 firms are from China, followed by seven each from India and Japan.

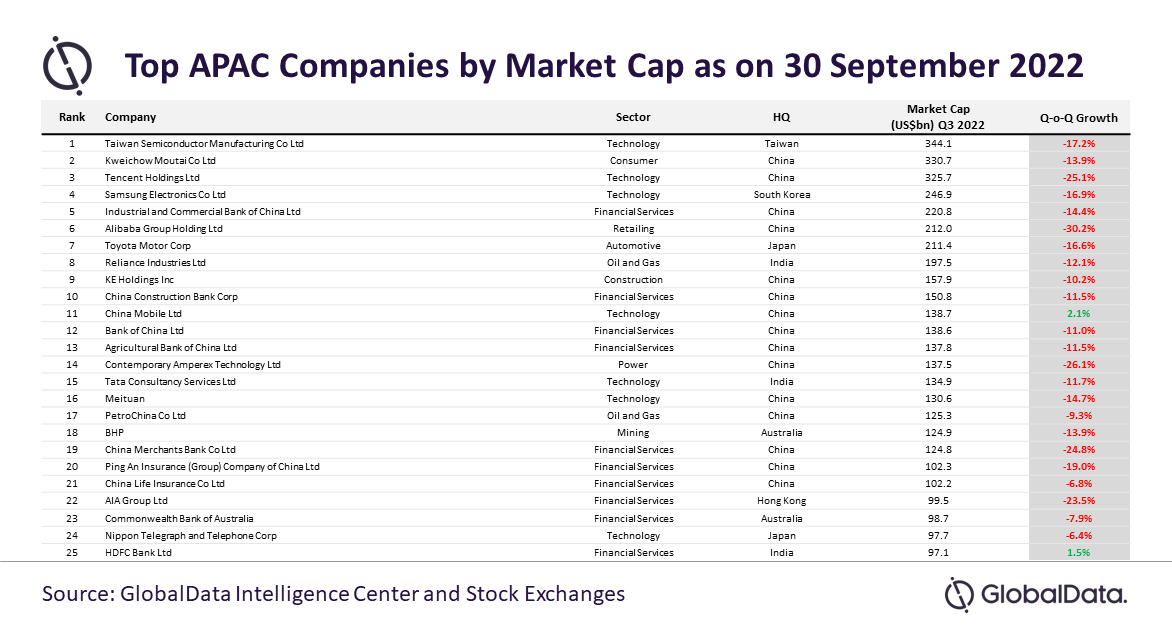

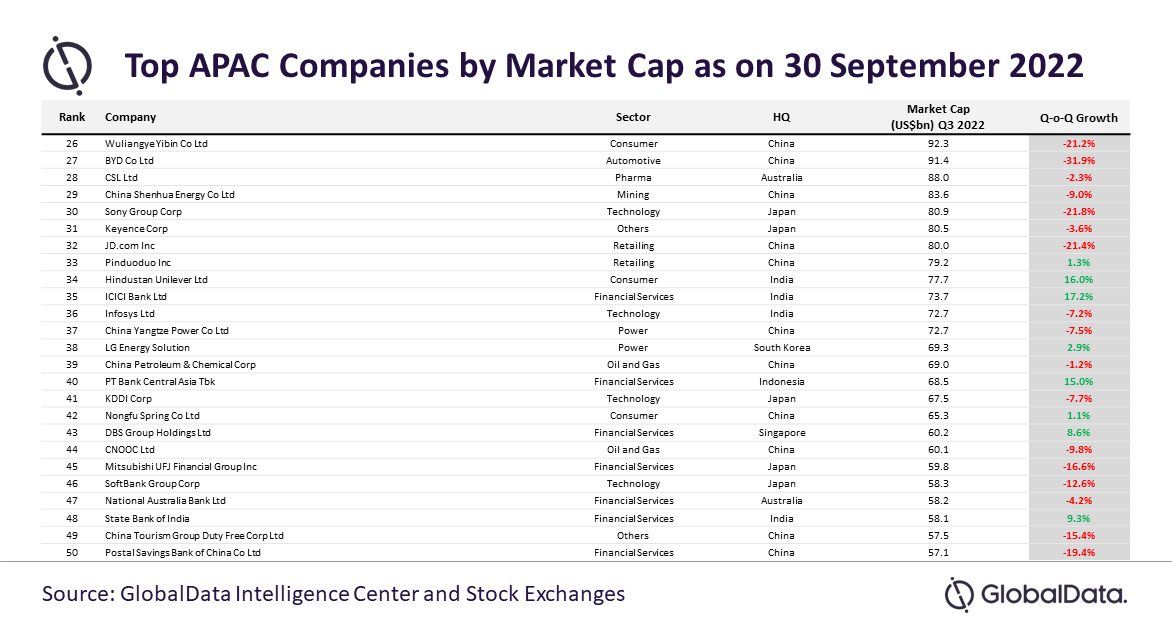

ICICI, Hindustan Unilever (HUL), and Bank Central Asia witnessed the highest quarter-on-quarter (Q-o-Q) growth, whereas Taiwan Semiconductor Manufacturing Company (TSMC), Kweichow Moutai, and Tencent were the leaders reporting more than $300 billion market capitalization (MCap). Leading Chinese firms BYD, Alibaba, and CATL witnessed their MCap eroding by 20%.

Sathiya Narayanan, Business Fundamentals Analyst at GlobalData, comments: “In Q3, 80% of the top 50 companies reported a decline in MCap from the previous quarter. Geo-political issues between the US and China over Taiwan, government regulations on tech stocks, and prolonged mass lockdowns impacted the Chinese market, especially firms such as BYD, Alibaba, Tencent and CATL.”

With speculations over Berkshire Hathaway’s reduction of its stake in BYD rife, a 32% decline in BYD’s valuation ensued during Q3. E-commerce giant Alibaba lost $91.5 billion in MCap due to supply chain constraints, concerns over delisting from the US stock market, and lower consumer spending. China Mobile, Pinduoduo, and Nongfu Spring were the bright spots among the Chinese companies, which reported growth in MCap during the period.

Among the Indian firms, Reliance, TCS, and Infosys lost 12.1%, 11.7%, and 7.2%, respectively, in Q3 2022, owing to the bearish trend in the equities market resulting in sell-off pressure among the investors.

Narayanan adds: “Despite Reliance Industries’ impressive FY2022 top-line performance, investors seemed to have lost confidence on the Indian conglomerate, because of the government’s tax imposition on the export of petrol and diesel to overseas markets by Indian companies. Overall, the quarter witnessed the company’s MCap declining by $27.1 billion.”

However, Indian financial services giants ICICI, SBI and HDFC recovered from the previous quarter’s slump with positive figures. HUL is the only Indian company on the list that witnessed growth in consecutive quarters.

None among the seven Japanese companies witnessed positive Q-o-Q growth and continued the declining trend. Tech stocks fell due to higher sell-off pressure among the investors amid the growing rift between China and the US over Taiwan and increasing inflation globally which impacted the risk appetite of investors.

Narayanan concludes: “Heightened uncertainty over the recession, COVID-19 lockdowns, supply-chain constraints, interest rate hikes, geo-political tensions, and inflation will have a negative impact on the APAC region’s MCap in Q4 2022 with the downtrend expected to continue in 2023.”

{kind=link}